The promise of Healthcare Transformation through digital technology is exciting but full of uncertainty. I predict that analytics will be most valued by the companies that pay for healthcare costs, rather than by the individuals who stand to benefit.

Verisk sells analytics products and services to companies to help these insurance payers and buyers minimize uncertainty, understand risks, and reduce costs. This focus allows Verisk Health to enjoy many strategic advantages but they face a threat of new entrants from start-ups who could pool and aggregate EMRs based on customers’ opt-in. Another threat is that when EMRs become ubiquitous, positive demand-side network effects could disrupt Verisk’s position.

Verisk should push the edge to the consumer to deepen lock-in with current customers and create value for new customers. Rather than marketing their product to consumers, Verisk would offer added B2C functionality through B2B clients. By adding this new value, Verisk’s clients’ patients and employees would demand continued service with Verisk.

Thursday, December 15, 2011

Wednesday, December 14, 2011

Siemens: Taking Old Business to New Business

One of Siemens core capabilities is energy automation innovation across the entire energy conversion chain which makes it possible to adapt power grids to future demands. In the future, Siemens needs to leverage these relationships to expand past the conversion chain to reach the end user. Through mergers, acquisitions and partnerships, Siemens can expand further into data analytics and consumer-facing services.

Read more about Siemens here.

Read more about Siemens here.

Tuesday, December 13, 2011

Final Insights on the Payment Processing Industry

Joe

The payment processing industry has slowly adapted available technology to combat fraud and streamline the experience for consumers. If the incumbents wish to remain so they must accelerate the implementation of new technologies or face the loss of marketshare and revenue to the likes of Google. As Paypal transformed the industry a few years ago Google is poised to repeat. Discover and American Express are in a unique position in the industry as not just network providers but also issuing banks. For Discover to continue to compete it must leverage customer data, like purchase and credit history to reduce bad debt and to increase revenues through savings and loan products.

Monica

Digital technologies have greatly impacted the payment processing industry, digital and mobile technologies have changed the way in which the industry works and will continue to do so in the future. The industry´s main players, like Visa and Mastercard, have had to develop digital capabilities most of them by acquisitions and partnering with companies that specialized in this areas. These technologies have opened up the industry to new players like Google which has led to a highly fragmented industry. It will be interesting to see how the industry consolidates and which players manage to gain leadership in the industry based on the development of their capabilities.

Burke

The credit card companies dominant positions in the payment industry is extremely vulnerable to the latest advances in digital technology. What’s to stop an Apple or Google from moving to the edge of payment processing and relegating a Visa or MasterCard to simply a back-end credit house? Paypal is also threatened by a new player called Dwolla, which provides an easy electronic payment solution at much cheaper rates. Dwolla is sure to spark imitators, and the whole industry could soon become commoditized.

Verifone is in good position with it’s industry-leading payment encryption technology, but the rest of their value-drivers (hardware, consulting, support) is really just complimentary. Verifone would be wise to week out strategic partnerships to ensure it’s place at the head of payment security providers.

Manoj

I see there are three distinct trends regarding payments.

One is the most obvious and very visible now - digital wallet, a now-common concept but used interchangeably with, but is different from, mobile payment. NFC is the enabling technology of this capability. Person-to-Person payment is an additional value driver.

Second, payment in virtual currency is a rapidly increasing trend. Coupons and reward points are familiar to us but with the advent of Facebook, Zynga, Groupon is really pushing this trend forward because you can now buy things with FB credit or use a virtual currency to make in-app purchase. This transaction does not require credit card networks and thus is taking significant value out of payment processing ecosystem. In my opinion, this is a big emerging threat to this industry which may be fundamentally disrupted by entities like Facebook.

Third, the concepts of network effects and platform strategy is so commonplace now that almost every single initiative taken by any player, big or small, has a kind of platform story to it. Google Wallet, American Express Serve, or Visa’s V.me - all these products blur the distinction between product, services and platform.The race to win the network effect is truly on among big players and it will take 3-4 years to know the winner. With ecommerce growing across the globe, the credit card networks may see a big change depending on who wins the global race of digital payment platform.

The payment processing industry has slowly adapted available technology to combat fraud and streamline the experience for consumers. If the incumbents wish to remain so they must accelerate the implementation of new technologies or face the loss of marketshare and revenue to the likes of Google. As Paypal transformed the industry a few years ago Google is poised to repeat. Discover and American Express are in a unique position in the industry as not just network providers but also issuing banks. For Discover to continue to compete it must leverage customer data, like purchase and credit history to reduce bad debt and to increase revenues through savings and loan products.

Monica

Digital technologies have greatly impacted the payment processing industry, digital and mobile technologies have changed the way in which the industry works and will continue to do so in the future. The industry´s main players, like Visa and Mastercard, have had to develop digital capabilities most of them by acquisitions and partnering with companies that specialized in this areas. These technologies have opened up the industry to new players like Google which has led to a highly fragmented industry. It will be interesting to see how the industry consolidates and which players manage to gain leadership in the industry based on the development of their capabilities.

Burke

The credit card companies dominant positions in the payment industry is extremely vulnerable to the latest advances in digital technology. What’s to stop an Apple or Google from moving to the edge of payment processing and relegating a Visa or MasterCard to simply a back-end credit house? Paypal is also threatened by a new player called Dwolla, which provides an easy electronic payment solution at much cheaper rates. Dwolla is sure to spark imitators, and the whole industry could soon become commoditized.

Verifone is in good position with it’s industry-leading payment encryption technology, but the rest of their value-drivers (hardware, consulting, support) is really just complimentary. Verifone would be wise to week out strategic partnerships to ensure it’s place at the head of payment security providers.

Manoj

I see there are three distinct trends regarding payments.

One is the most obvious and very visible now - digital wallet, a now-common concept but used interchangeably with, but is different from, mobile payment. NFC is the enabling technology of this capability. Person-to-Person payment is an additional value driver.

Second, payment in virtual currency is a rapidly increasing trend. Coupons and reward points are familiar to us but with the advent of Facebook, Zynga, Groupon is really pushing this trend forward because you can now buy things with FB credit or use a virtual currency to make in-app purchase. This transaction does not require credit card networks and thus is taking significant value out of payment processing ecosystem. In my opinion, this is a big emerging threat to this industry which may be fundamentally disrupted by entities like Facebook.

Third, the concepts of network effects and platform strategy is so commonplace now that almost every single initiative taken by any player, big or small, has a kind of platform story to it. Google Wallet, American Express Serve, or Visa’s V.me - all these products blur the distinction between product, services and platform.The race to win the network effect is truly on among big players and it will take 3-4 years to know the winner. With ecommerce growing across the globe, the credit card networks may see a big change depending on who wins the global race of digital payment platform.

Monday, December 12, 2011

Education Sector Final Deliverables

Click on the word cloud to travel to the IS714 "Education Sector" Google Site, containing both our group and individual project work including:

- Final industry network diagram: As well analysis and insights on how technology is shaping how industry participants interact in this sector

- Expanded individual company analysis: Assessment of core capabilities, strategies for future growth, and key partnerships moving forward.

PG&E Capabilities

PG&E needs to embrace digital technology as a way to engage their customers. This is important because it solves two problems.

First, demand for electricity is increasing and customers don't want more transmission lines to be built near their homes. PG&E can use the technology that SmartMeters provide in order to implement time of use programs that will incentivize customers to use less energy during periods of high demand.

Second, customers often have inefficient behavior that is causing an unstable grid. By partnering with Nest Learning Thermostat, PG&E can use technology to influence consumer behavior.

More details can be found in these slides.

First, demand for electricity is increasing and customers don't want more transmission lines to be built near their homes. PG&E can use the technology that SmartMeters provide in order to implement time of use programs that will incentivize customers to use less energy during periods of high demand.

Second, customers often have inefficient behavior that is causing an unstable grid. By partnering with Nest Learning Thermostat, PG&E can use technology to influence consumer behavior.

More details can be found in these slides.

Allscripts Capabilities

http://prezi.com/cqmzkgs0iwsg/allscripts-capabilities/

Above are a few slides about capabilities at Allscripts. Allscripts is currently the largest provider of practice management and electronic medical record technologies with over 180,000 providers on their platform. They have a reputation for being innovative in their design of offering integrates solutions for clinical, financial and administrative functions.

In order to remain competitive, I think that Allscripts needs to expand their customer base to include smaller hospitals and private practices. To do this, they will need to embrace modularity and customer flexibility, allowing customers to choose just the services they want, rather than the entire EMR system. Giving customers a pay-as-you-go model will allow organizations to use Allscripts without the large capital investment that is currently necessary.

I also think that Allscripts should push the edge out to the patient. Currently Allscripts views healthcare providers as their customers, but value can be added by bringing the healthcare platform to the patient. Legislation and trends in the industry are demanding a more patient-centric approach. This doesn't just mean hospitals; it means IT companies too.

Report on Big Data Analytics

Big data analytics is where advanced analytic techniques operate on big data. This report came out a couple of months ago on how companies are coping with applying data analytics to large data sets.

Sunday, December 11, 2011

Amazon, the Company That is Taking Over Digital Media

A colossal attack is currently underway by the large technology giants, on the already highly saturated and mature pay TV market. The pay TV market, dominated by traditional cable and satellite TV providers, is quickly transforming, as major players enter the market. In addition to the wider selection offered on various devices through digital media, as economic conditions put financial pressure on households, consumers are looking for more affordable options. In addition to the concentrated pay TV market, the entire digital media industry is highly saturated (see Figure 1 below).

Figure 1

The ability to capture value, access content, and build and maintain partnerships will continue to be critical to the success of players in this industry. The digital media industry is dominated by major conglomerates, with companies having several different core capabilities; consequently, this industry is highly inter-connected.

Amazon, a member of the Gang of Four, is well positioned not only to strengthen its position in the tech gang. Originally introduced with the bold mission to become the “Earth’s largest bookstore,” the company has quickly evolved to become a leader in ecommerce, physical and digital distribution, ebook publishing, and now digital media ecosystem creation. As some argue that Amazon is copying Apple’s strategy, Amazon has the tv and video content, ever increasing, through Amazon Prime, and the device(s), through the Kindle Fire and rumored Amazon phone. To target a different, larger market, Amazon competes in a way where it is and always has been “very comfortable operating at extremely low margins.”

So where is Amazon headed? As can be seen in the stack model (Figure 1), Amazon is already a significant player in four of the five major digital media industry layers. Will Amazon choose to venture into tv and video content creation and production, similar to how it disrupted the publishing industry? Or will it choose to continue to focus on building its ecosystem, through device(s)?

Considering the McKinsey Quarterly on the “Ten tech-enabled business trends to watch,” Amazon appears to be taking the approach of “imagining anything as a service.” Amazon is not only using its platform as a service but adding to its services through content and devices. Amazon’s core capability is servicing the world by connecting the world. Amazon has already done this in the publishing industry, successfully finding and supporting people or talent to create new material, supported by the process of connecting third party retailers, technology allowing digital publishing and storage in the cloud, and organization that ensures low prices.

With digital media, specifically tv and video, Amazon will likely take this opportunity to truly provide an all-in-one service that locks in customers. Amazon is in a very unique position where it has vast amounts of information on consumers, related to music, books, videos, and devices, to be used in experimentation through big data; similarly, it already is highly connected to or servicing consumers, sellers, and enterprises. The technology is already there, with analytics to understand the viewer and provide valuable information to the producer, along with Amazon Cloud Drive, ensuring anywhere access to consumers. The organization will be consistent with Amazon’s focus on wide selection, low price, and convenience, continuing to connect customers and other players, from content creators to OTT service providers. Finally, the process will be interesting, as it expands Amazon’s ability to be more than an etailer, distributor, and publisher, but also a manufacturer, and ultimately, an entire ecosystem provider. It is critical to remember that “Content is King!” As it has already done in publishing, Amazon needs to support independent content creation by identifying and support talent, with a process to incentivize these creators, to take advantage of the long-tail opportunities. With easy access to capital to further invest in acquiring, licensing, and/or creating content, Amazon must continue its recent efforts of building and maintaining relationships with the major content producers, to guarantee the latest and most in demand content.

Microsoft Health Solutions Group - Capabilities Analysis

In order to create a better system design, Microsoft needs to understand the layers in the

Health sector and in a sense, define the layers to suit the information flow. As shown in the presentation below, it is important for Microsoft to understand the key stake holders and also factor in the global delivery and support which will be a key to success with lots of information flow across geographies resulting from frequent migration of people between countries. At every layer, Microsoft needs to build capability to define a key control point and focus on defining and driving the layer with that capability.

The Healthsector Information system is most certainly moving towards being a two sided market. Microsoft will need to build its capabilities in two delivery channels. B2B with the customers being major Hospitals, Insurance companies and the Life Sciences organizations. On the other hand, Once these capabilities are built, It can build capabilities to monetize its B2B capabilities by extending it to B2C channels by targeting the actual patients. The key capabilities are going to be in terms of Technology for B2B and in terms of Process definition in terms of B2C channels.

For B2B channels, Microsoft needs to build its data management capabilities and also build its capabilities in terms of data security and Access Management

For the B2C channels, It is important that Microsoft defines specific processes in terms of App development. Support on Windows or a proprietary robust operating system and also the process for app selection, SDK delivery will be critical. In terms of the end users, it will be important to monitor the devices on which the apps are being installed in order to ensure that the backend data security and other capabilities are delivered optimally.

Please visit our site for a comprehensive analysis of the industry and the different firms.

http://healthsector-714.weebly.com/index.html

Insights and Learning from the Video Game Industry.

The following are the insights about the Gaming Industry characteristics, opportunities and threats from 2011 to 2016, studied from the different perspectives of six established incumbents in the sector.

Insights from Carl about the Gaming Industry and Sony:

As we make progress in technology and gaming consoles become more similar, the battle is going to shift to content creation even more. This is the only true way that gaming giants like Sony will be able to survive. Consoles are a means to play games, and for the most part, a loss-making enterprise.

Nintendo has a proven track record of creating great games that are only sold on their console. This is one of the main reasons that they own the biggest market share of console sales*. XBOX and Sony have been sharing some of the best game developers for quite a while and this has cost them in market share.

Immersive gameplay will also be a big differentiator because of the different approaches that the console manufacturers have taken to enter this market. So far, Nintendo has the first-mover advantage, but Microsoft has created a wholesome solution with the Kinect and will be able to revolutionize the market once again, especially since they have integrated the system into their home entertainment system and beat Apple in creating the next generation “TV.” Sony’s solution is lackluster.

Having said that, Sony just released one of the best commercials I have seen (http://www.youtube.com/watch?v=mdWkKKSckNk) in a while and this has signaled to me that they are not ready to give up, and that they are turning to their partners for exclusive game content. They have an uphill battle against Nintendo and Microsoft, but they have years of experience, deep pockets, and some pretty loyal fans of the PS2 era. I will be glad to be an observer for the next five years and enjoy the benefits of these giants competing.

*Thormahlen, C. IBISWorld Industry Report NN003, Video Games in the US. IBISWorld, March 2011

Insights from Elana Horowitz

As players in the video game industry struggle to find mindshare in a day and age when there is no shortage of titles and platforms, they will have to think of new ways to differentiate themselves. While some such as XBOX have connected to the world of television, others like Nintendo have penetrated the education market. Companies that originated in one layer are now integrating vertically, both up and down, in their stacks to offer a more comprehensive tool. Soon enough each layer with be completely saturated with hundreds of players that occupy all levels.

Much like Apple, the company that will eventually be declared the winner will demonstrate creativity in developing a new layer. A visionary company will come in and find a way to monetize an extended feature of video games in a way that will gain them a first mover advantage in the space. As the demographic of gamers expands, this task becomes more difficult and easier at the same time. The gaming company will need to fulfill the demands of an extremely diverse group but will also have more options to consider which is great for the creative process. It is also very likely that the technologies that will facilitate further layer expansion have yet to be developed.

Insights about GameStop from Akshay Shah

As we look at the network model for the gaming industry over the next few years, a few trends emerge. Even over the past five years, more firms who were traditionally platform providers or content creators have moved into distribution, leveraged by content digitization and with the strategic goal of cutting the middle man . We have seen companies such as Microsoft, Apple, and Nintendo develop direct consumer relationships -- areas once controlled by GameStop, Target, and other brick and mortar retail stores. We have seen this play out in the music industry and more recently with ebooks.

GameStop, however, is not seeing these trends. For example, it is continuing to purchase real estate to build new retail locations. One of the core competencies I identified during the mid-semester analysis was GameStop’s familiarity with its customers. As customers move to digital products on digital platforms, GameStop will lose its relevance. Though there is still time while physical content is still being consumed, they need to act quickly as services such as GameFly can potentially do to them what Netflix did to Blockbuster.

Insights from Paul Taylor

Creative and inspiring content is becoming the driving force in the gaming industry, but it is also the biggest struggle for many game developers. There is enormous pressure from game enthusiasts as well as console manufacturers for developers to create the next “Mario”, “Halo”, and “World of Warcraft”. However, there are enormous costs associated with bringing games to market that developers are not venturing to undertake that risk. More often than not, successful IP is similar to the idiom “even a blind squirrel can find a nut” because success is often unexpected. Buildup and expectations for games are so great that many fail to live up to them and a sequel will never see the light of day. Once IP has a successful following, the developer and publisher will continue to milk that franchise for as long as possible hoping that the content will never become stale. The two giants in the software and publishing layer, Electronic Arts and Activision Blizzard, have released several iterations of popular franchises like Call of Duty, Guitar Hero, and Madden Football. This strategy is not sustainable and there is now an opportunity for the rise of a new layer.

Fortunately, or unfortunately depending on the perspective, a new layer has emerged that will become a major player in the future of gaming, which is Mobile and Online Gaming. The game developers in this layer have a much different business model and are able to produce original content at much smaller costs. Not only do they have to pay the enormous licensing fees that console manufacturers are charging for SDKs, but they can publish their games on platforms like Apple’s App Store and the Android Market for the fraction of the cost. As a result, they are able to charge a significantly reduced price to consumers. This trend already struck fear into one long established giant. Nintendo has lashed out at developers for selling games for only $0.99 and vowed that they will never release their content on the mobile platform. While this is seen as a move to protect their interests, Nintendo has already recognized this movement as a threat to their long-term viability in gaming. It will be interesting to see how the next 5 years play out in this sector…

Insights from Todd Valentine

This industry is posed for significant change in the next 5 years, and competition between the big players in the industry will dictate the nature of the industry in 2016. Consistently delivering value to consumers in regular cycles will enable the console manufacturers to capture a larger slice of the market, and developers will follow the console manufacturer with the largest audience and best developer tools.

Insights from Humberto Silva

The Gaming industry, as other Information businesses industries, is experiencing a significant change with the disappearance of the physical media and the advent of social media and cloud computing. This trends disrupted the field changing the rules of the game and the different balances of power and influence across the value chain. New layers has emerged -online distribution and social media- and the older ones -content development and brick and mortar distribution- keep losing ground.

Almost all the big players in the industry have reacted trying to adapt their long term strategies. Electronic Arts, the 2nd biggest content creator and distributor in the video games sector acknowledge the transformation of the business deciding to focus their effort in create Origin, a online digital store they expect to become a platform for content distribution, while investing in the social media gaming arena through mergers & acquisitions, Popcap Studio was acquire by EA in early 2011 for S1.3B (a third of EA’s current revenues).

I believe EA strategy is adequate because it is focused on the current trends. However this industry have been always leaded by innovations, either in hardware or software. Incorporating an statement about the importance of the innovation process EA could strengthen it current position in the video games battlefield.

The following are the insights about the Gaming Industry characteristics, opportunities and threats from 2011 to 2016, studied from the different perspectives of six established incumbents in the sector.

Insights from Carl about the Gaming Industry and Sony:

As we make progress in technology and gaming consoles become more similar, the battle is going to shift to content creation even more. This is the only true way that gaming giants like Sony will be able to survive. Consoles are a means to play games, and for the most part, a loss-making enterprise.

Nintendo has a proven track record of creating great games that are only sold on their console. This is one of the main reasons that they own the biggest market share of console sales*. XBOX and Sony have been sharing some of the best game developers for quite a while and this has cost them in market share.

Immersive gameplay will also be a big differentiator because of the different approaches that the console manufacturers have taken to enter this market. So far, Nintendo has the first-mover advantage, but Microsoft has created a wholesome solution with the Kinect and will be able to revolutionize the market once again, especially since they have integrated the system into their home entertainment system and beat Apple in creating the next generation “TV.” Sony’s solution is lackluster.

Having said that, Sony just released one of the best commercials I have seen (http://www.youtube.com/watch?v=mdWkKKSckNk) in a while and this has signaled to me that they are not ready to give up, and that they are turning to their partners for exclusive game content. They have an uphill battle against Nintendo and Microsoft, but they have years of experience, deep pockets, and some pretty loyal fans of the PS2 era. I will be glad to be an observer for the next five years and enjoy the benefits of these giants competing.

*Thormahlen, C. IBISWorld Industry Report NN003, Video Games in the US. IBISWorld, March 2011

Insights from Elana Horowitz

As players in the video game industry struggle to find mindshare in a day and age when there is no shortage of titles and platforms, they will have to think of new ways to differentiate themselves. While some such as XBOX have connected to the world of television, others like Nintendo have penetrated the education market. Companies that originated in one layer are now integrating vertically, both up and down, in their stacks to offer a more comprehensive tool. Soon enough each layer with be completely saturated with hundreds of players that occupy all levels.

Much like Apple, the company that will eventually be declared the winner will demonstrate creativity in developing a new layer. A visionary company will come in and find a way to monetize an extended feature of video games in a way that will gain them a first mover advantage in the space. As the demographic of gamers expands, this task becomes more difficult and easier at the same time. The gaming company will need to fulfill the demands of an extremely diverse group but will also have more options to consider which is great for the creative process. It is also very likely that the technologies that will facilitate further layer expansion have yet to be developed.

Insights about GameStop from Akshay Shah

As we look at the network model for the gaming industry over the next few years, a few trends emerge. Even over the past five years, more firms who were traditionally platform providers or content creators have moved into distribution, leveraged by content digitization and with the strategic goal of cutting the middle man . We have seen companies such as Microsoft, Apple, and Nintendo develop direct consumer relationships -- areas once controlled by GameStop, Target, and other brick and mortar retail stores. We have seen this play out in the music industry and more recently with ebooks.

GameStop, however, is not seeing these trends. For example, it is continuing to purchase real estate to build new retail locations. One of the core competencies I identified during the mid-semester analysis was GameStop’s familiarity with its customers. As customers move to digital products on digital platforms, GameStop will lose its relevance. Though there is still time while physical content is still being consumed, they need to act quickly as services such as GameFly can potentially do to them what Netflix did to Blockbuster.

Insights from Paul Taylor

Creative and inspiring content is becoming the driving force in the gaming industry, but it is also the biggest struggle for many game developers. There is enormous pressure from game enthusiasts as well as console manufacturers for developers to create the next “Mario”, “Halo”, and “World of Warcraft”. However, there are enormous costs associated with bringing games to market that developers are not venturing to undertake that risk. More often than not, successful IP is similar to the idiom “even a blind squirrel can find a nut” because success is often unexpected. Buildup and expectations for games are so great that many fail to live up to them and a sequel will never see the light of day. Once IP has a successful following, the developer and publisher will continue to milk that franchise for as long as possible hoping that the content will never become stale. The two giants in the software and publishing layer, Electronic Arts and Activision Blizzard, have released several iterations of popular franchises like Call of Duty, Guitar Hero, and Madden Football. This strategy is not sustainable and there is now an opportunity for the rise of a new layer.

Fortunately, or unfortunately depending on the perspective, a new layer has emerged that will become a major player in the future of gaming, which is Mobile and Online Gaming. The game developers in this layer have a much different business model and are able to produce original content at much smaller costs. Not only do they have to pay the enormous licensing fees that console manufacturers are charging for SDKs, but they can publish their games on platforms like Apple’s App Store and the Android Market for the fraction of the cost. As a result, they are able to charge a significantly reduced price to consumers. This trend already struck fear into one long established giant. Nintendo has lashed out at developers for selling games for only $0.99 and vowed that they will never release their content on the mobile platform. While this is seen as a move to protect their interests, Nintendo has already recognized this movement as a threat to their long-term viability in gaming. It will be interesting to see how the next 5 years play out in this sector…

Insights from Todd Valentine

This industry is posed for significant change in the next 5 years, and competition between the big players in the industry will dictate the nature of the industry in 2016. Consistently delivering value to consumers in regular cycles will enable the console manufacturers to capture a larger slice of the market, and developers will follow the console manufacturer with the largest audience and best developer tools.

Insights from Humberto Silva

The Gaming industry, as other Information businesses industries, is experiencing a significant change with the disappearance of the physical media and the advent of social media and cloud computing. This trends disrupted the field changing the rules of the game and the different balances of power and influence across the value chain. New layers has emerged -online distribution and social media- and the older ones -content development and brick and mortar distribution- keep losing ground.

Almost all the big players in the industry have reacted trying to adapt their long term strategies. Electronic Arts, the 2nd biggest content creator and distributor in the video games sector acknowledge the transformation of the business deciding to focus their effort in create Origin, a online digital store they expect to become a platform for content distribution, while investing in the social media gaming arena through mergers & acquisitions, Popcap Studio was acquire by EA in early 2011 for S1.3B (a third of EA’s current revenues).

I believe EA strategy is adequate because it is focused on the current trends. However this industry have been always leaded by innovations, either in hardware or software. Incorporating an statement about the importance of the innovation process EA could strengthen it current position in the video games battlefield.

EMR Growth rate

This short article agrees with what I posted in a previous blog. The EMR is rapidly growing.

EMR market value was $15.7 billion in 2010 and its growth rate was 10% in 2009 and increased to 13.6% in 2010.

This can be considered, by all means, an astonishing growth rate. Yet, much less than what was previously expected.

The article predicts that the growth rate will rapidly increase in the nearby future.

http://www.fierceemr.com/story/emr-market-expected-increase-growth/2011-03-03

EMR market value was $15.7 billion in 2010 and its growth rate was 10% in 2009 and increased to 13.6% in 2010.

This can be considered, by all means, an astonishing growth rate. Yet, much less than what was previously expected.

The article predicts that the growth rate will rapidly increase in the nearby future.

http://www.fierceemr.com/story/emr-market-expected-increase-growth/2011-03-03

Amazon had been successful in capitalizing on its digital publishing and mobile device technology capabilities to develop a strong foot hold within the educational sector. However, traditional publishers responded by consolidating, capitalizing on their relations and developing digital capabilities.

Currently a new wave of disruption is impacting the industry, namely web 2.0 and collaboration technologies. Could this technologies really rewire our educational system and transform it from a one to many model in to a more customized many to many model? And how could Amazon react to that?

Check out our recommendation to know the answer to those questions:

http://portal.sliderocket.com/BAXEB/Amazon1212

Currently a new wave of disruption is impacting the industry, namely web 2.0 and collaboration technologies. Could this technologies really rewire our educational system and transform it from a one to many model in to a more customized many to many model? And how could Amazon react to that?

Check out our recommendation to know the answer to those questions:

http://portal.sliderocket.com/BAXEB/Amazon1212

Digital Media Network Analysis and Lessons Learned

Network Analysis

Please enjoy the following presentation on our network analysis of the Digital Media and Entertainment industry. We manipulated the network diagrams to better demonstrate the ties between layers in our stack model, which we found to deliver some great insights into the complexity of this industry.

A class assignment in Networks

View more presentations from efhansen.

Lessons Learned

Given that the Digital Media industry stack has changed significantly over the last five years, with new players in OTT services, new avenues of distribution (digital v. physical), and a new platform layer that is ever evolving, the landscape and subsequent industry stack is sure to change again in the next five years.

Here are some lessons that we learned throughout the semester:

- The digital media industry is in constant flux. With each new innovation or change, the entire industry shifts (Hulu is a great example of this). Firms in the industry must always be looking forward and be willing to take calculated risks in order to keep up.

- Networks and studios are developing both vertically and horizontally to cover all bases as the industry transforms. We anticipate a move to extradite themselves from the ventures that do not prove to be effective and over the next few years shift back down to their core capabilities. Tech giants Amazon, Apple, and Google may have an advantage, as their core capabilities tend to naturally span horizontally across multiple layers.

- Incorporation of analytics and customization of content to mobile devices will certainly continue to shape this industry.

- Content producers are joining the online streaming game, and will likely stop licensing (or increase license fees) with 3rd party OTT services once they have built the requisite capabilities (and/or user base) to offer content directly to consumers.

- The network for the industry is still missing a few links between hardware and content producers. Networks and studios should develop their own streaming capabilities in order to protect and improve margins on their original and library content.

- Defining capabilities, industry networks, and stack models is more of an art (design) than a science, since different choices must be made depending on the level from which it is viewed (such as the firm or industry)

Identity, Security and Privacy in the Gaming Sector

Identity

Security

Privacy

Privacy in video games is a challenge for game developers, console manufacturers, and consumers. Consumers could have their gaming experience in complete isolation and experience privacy, but the value added from having a connected gaming experience drives most gamers to open communication channels. The challenge then for the game developers and console manufacturers is to ensure privacy controls within the connected gaming experience.

For example, Microsoft Xbox Live shows a when a user is logged in, their achievements, the game they are playing or the movie they are watching at that time. Users are prompted upon first setting up their Xbox Live account to enable or disable this feature, and the choice can be changed at any time. The result is a value added connected gaming experience while enabling consumers to have a finer degree of control over their information.

The changes in the cloud computing era will also impact privacy in video games. Microsoft recently enabled cloud storage for game saves (http://www.youtube.com/watch?v=g77UF5tGfm8). This requires consumers to sacrifice a bit of their privacy for added value in a balance that Microsoft must consistently deliver.

In the past decade, video game characters have become moldable and specific to the user. During the early years of simple computer games and the original Mario & Luigi, gamers had the option to select from a variety of pre-developed characters. Gamers could identify with certain characters or simply pick a favorite, and adopt them as their own for use at every new game. Choices were finite.

As video game structures have changed from short epics to longer, complex levels, video game makers have given gamers the opportunity to design themselves in their virtual worlds. With the advent of Wii, gamers were encouraged to model themselves as a cartoon, choosing, for example, hair color and style. As technology advances and graphics improve, gamers will get the opportunity to create avatars that are the spitting images of the real thing. There is tremendous potential to use such technology to educate individuals and influence behavior. For example, if someone creates a character with the same body proportions, goes on a binge eating rampage in the game and sees the results, an obese man who has difficulty completing tasks within the game, the individual might rethink how he conducts his real life. Seeing yourself and the effects of your choices on screen can send a powerful message.

Also, with interactive gaming gaining popularity, gamers will are able to modify their identities to project a persona that they wish to have rather than what the reality of the physical world dictates. Their virtual lives can serve as an escape from reality, where they can experiment, test, and revert to their ideal state with the click of a button.

Security

Security in gaming came to the forefront and turned into a mainstream issue with news of a security breach of Sony’s PlayStation Network by a group of hackers that shut down the service for nearly a month and ultimately cost Sony millions of dollars in revenue and damage to the PlayStation brand. This security breach is now the largest breach in history with over 77 million accounts compromised, which surpassed the TJX security incident back in 2007 (http://en.wikipedia.org/wiki/PlayStation_Network_outage). Incidents similar to Sony’s will continue to occur in the sector for the foreseeable future, although at a much smaller scale, now that gaming has entered the digital era and online accessed content and platforms become ubiquitous. The spotlight is now brighter than ever on security in the gaming sector as Sony is still recovering from this incident, but security has always been an issue for all companies that are associated with gaming.

Security is a blanket statement in gaming because there are so many different contexts where security is applicable. Some examples include manipulating code in games, accessing online game servers, cheating to obtain an advantage, assuming another gamer’s identity, and so on. These are just a few examples, but the reality is that compromises in security can have a profound adverse effect in this sector compared to the other sectors where security may not be as vital. Game developers and publishers can lose millions with pirated software while gamers can become frustrated and lose interest when other gamers cheat to gain a competitive advantage in online video games. For the most part, security has been adequate in the gaming sector up to this point but the PlayStation incident brought the sector to its knees. While that incident was devastating to Sony and the PlayStation brand, it will serve as a reminder to the rest of the industry that security is going to play a major issue in the future and that companies must do everything they can to mitigate that risk. The digital era will usher in additional challenges and unforeseen risks that all companies must grasp or face a similar outcome that Sony experienced earlier this year.

Privacy

Privacy in video games is a challenge for game developers, console manufacturers, and consumers. Consumers could have their gaming experience in complete isolation and experience privacy, but the value added from having a connected gaming experience drives most gamers to open communication channels. The challenge then for the game developers and console manufacturers is to ensure privacy controls within the connected gaming experience.

For example, Microsoft Xbox Live shows a when a user is logged in, their achievements, the game they are playing or the movie they are watching at that time. Users are prompted upon first setting up their Xbox Live account to enable or disable this feature, and the choice can be changed at any time. The result is a value added connected gaming experience while enabling consumers to have a finer degree of control over their information.

The changes in the cloud computing era will also impact privacy in video games. Microsoft recently enabled cloud storage for game saves (http://www.youtube.com/watch?v=g77UF5tGfm8). This requires consumers to sacrifice a bit of their privacy for added value in a balance that Microsoft must consistently deliver.

Some basics in HIT

Since the late 1990’s, healthcare delivery organizations have undergone major initiatives to adopt health information technology (HIT). These initiatives have significant potential to improve patient safety, organizational efficiency and patient satisfaction. As of 2009 however, only 2% of non-federal hospitals had a comprehensive electronic health record (EHR), with another 7.6% using a basic EHR. The EHRs are most commonly used for electronic viewing of labs, reports, and images. In addition, one in five hospitals reported a fully implemented computerized order entry and clinical decision support.

There has been a large amount of legislation recently to foster widespread use of HIT. Between 2005 and 2008, a total of 168 pieces of HIT related legislation were passed by state governments. In addition, the Health Information Technology Economic and Clinical Health Act (HITECH) of the American Recovery and Reinvestment Act (ARRA) of 2009 is providing unprecedented opportunities to expand HIT efforts through grants, loans and financial assistance programs. The legislation also mandates “meaningful use” of an EHR.

Despite the opportunities and support, many hospitals struggle to implement HIT. Inadequate capital is the most common barrier to adoption in hospitals. Other reasons include unclear ROI, maintenance cost, physician resistance and inadequate IT staff. Cloud computing, which has grown in popularity in other industries, could provide a way for healthcare delivery organizations to overcome these barriers.

Saturday, December 10, 2011

Insights from Revised Education Sector Network Diagram

For our final network diagram of the education sector, our team’s goal was to create a true bipartite diagram mapping key education sub-sector industries against the involvement of our individual companies and their competitors. We then employed a node layout that helped to identify the relative positioning of the sub-sector industries. Node size is determined by number of connected edges (we initially attempted sizing nodes by sub-sector industry revenue but Institutional Delivery at $456B unacceptably skewed the scale). This more focused approach resulted in a far more useful visualization of the education sector, and led to the following insights:

- The relative size of eLearning/Collaboration shows its current and future importance in education work. It is clear that if universities do not adopt eLearning methods, they risk being marginalized (as the eLearning node did not even exist 15 years ago).

- There are relative groupings of several education sub-sector industries, in particular the more traditional industries of Traditional Publishing, Physical Distribution, and Retailer.

- There is a strong relationship between companies and organizations engaged in Institutional Delivery and eLearning / Collaboration.

- Digital Publishing is primarily made up of companies that are in Traditional Publishing.

- Sub-sector industries on the periphery include Devices and Education Policy.

- School Management and Testing/Assessment include nearly the same companies. If a particular company is in one but not the other, it would be a natural area for them to expand their operations.

- Testing / Assessment have fewer players, indicating a dependence on governmental policies (i.e. if a policy shifts or a new technology allows a policy shift, companies in that space may need to rapidly update their product offerings).

What if cars drive themselves !

"Moore's Law, first predicted in the 1970’s, talks about the long-term exponential growth of technology. It states that the performance of a computer’s central processing unit (CPU) consistently doubles every 2 years. This means that by the year 2030, the average mass-market computer chip will be 1024 times more powerful than the average computer chip in 2010. It also means that a single computer chip will be able to do more computations per second than the human brain itself." Sounds frightening but is very much a possibility. Though there could be the "Matrix effect" or other implications, this also means that you can let chips drive your car and not break your head on traffic chaos, believes the Japanese students working on the Autonomy concept.

http://www.behance.net/gallery/Autonomo-2030-Concept-Autonomous-Mobility/2422404

Interesting..but is it possible ? "Nothing is impossible" says our education..let us wait and see.

Thursday, December 8, 2011

If there remains lingering doubt that =everything= will move to the cloud...

In spite of terminal service applications such as Citrix, I have heard the argument that high-end applications such as Photoshop and AutoCAD won't work in the cloud, necessitating workstation-class PCs, at least for some people, essentially forever.

This site is early proof that that idea may not be accurate. It allows you to stream relatively recent games to your PC, Mac, TV or iPad (with iPhone support coming soon), fullscreen, with pretty good detail and frame rates. I downloaded the free client and experimented some and I have to say it works much better than I had expected. You get pretty high resolution streaming gaming content, which reacts to your input without much lag. It's not quite the experience that a high-power computer delivers, but given a fast internet connection, it's dangerously close. If you're a gamer, it's worth checking out. $10 / month for access to a growing list of games (currently at over 100) isn't a bad deal.

I'm talking about the Spotification of games! As a concept, I think it's pretty cool.

Of course, this doesn't address the problem of international laws and cross-boarder data transfers, but the "performance" argument seems to be breaking down.

In the future, as more and more high-performance applications move to the cloud I can imagine the concept of Chrome Books catching on more dramatically, even as home PCs. Alternately, the holy grail idea of having the same desktop experience on any computer worldwide could actually be realized (here's hoping).

Energy Sector Data Analytics

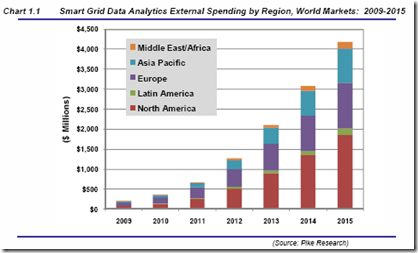

As we mentioned in our previous analysis, one of the key benefits of the Smart Grid, beyond its 2-way communication ability, is the vast amounts of data about usage it will provide. The problem is, what do we do with all that information? If we think about, in the near future, every electric outlet or piece of equipment connected to an electric outlet within a house will be able to communicate back to the utility how much energy it uses, and how and when it uses it. If we multiply this by the number of times a measurement can be made (and the more often this is done, the better), then by the number of houses in a city or a region and then we merge this data with all the data coming from other cities and regions, we will have an enormous quantity of data, that not only needs to be transported and stored, but also, and more importantly, analyzed.

According to Pike Research, the yearly worldwide spending on data analytics for the Smart Grid will reach $4.2B by 2015:

According to Pike Research, the yearly worldwide spending on data analytics for the Smart Grid will reach $4.2B by 2015:

Although these are big numbers, there won’t be space for everybody. Big players like SAS and IBM will tend to buy smaller companies to complement their offering, while smaller players will either devote their efforts to focus in niche applications, or will join forces to create a new player. Whatever the outcome, one thing is clear: data analytics will be one of the pillars for the Smart Grid.

Updated Gaming Bipartite Network

Updated Network Insights

As we look at the network model for the gaming industry over the next few years, a few trends emerge. Even over the past five years, more firms who were traditionally platform providers or content creators have moved into distribution, leveraged by content digitization and with the strategic goal of cutting the middle man. We have seen companies such as Microsoft, Apple, and Nintendo develop direct consumer relationships -- areas once controlled by GameStop, Target, and other brick and mortar retail stores. We have seen this play out in the music industry and more recently with ebooks.

Also as a result of the digitization of video games, it is becoming easier for new content creators ("indie studios") to reach an audience. The gaming platforms that are being developed also require a less formal knowledge structure to begin development. For example, the mobile gaming SDKs have a lower learning curve than the more robust XBOX or PlayStation SDKs. These dynamics have led to a proliferation of smaller independent video game development firms, who can create and deliver a video game with as little as one person -- a feat that was impossible as recently as five years ago.

All this trends are visible in our network of relation of the industry. When analyzing the network big picture it is interesting to observe that the bigger players in the Industry - Microsoft, Sony, Nintendo - are positioned in a central node that allow them to oversee the industry and influence in the different layers. Also is remarkable how heterogeneous the game development layer is. With game studios, movie makers and brands interacting for the content development creation.

In our view in the near future this network will continue its expansion towards the online and social gaming layers, those companies able to effectively incorporate this new trends in their value chain will prevail in the market. At the same time content creation will become even more competed since technology has increase the availability of tools for creative small player and also has lowered development cost.

Smart Grid Partnerships

As we learned in class, when digitalization is

central to core capabilities, vertical integration moves further away from

economies-of-scale achieving lower costs, and instead, we see

“economies-of-expertise” appearing through integrating portfolios of

capabilities through relationships. In short, companies are partnering or

merging together in order to encompass more of the industry.

The Smart Grid industry has seen a lot of this.

As discussed in our previous analysis, one of the interesting things we’ve seen

in analyzing the Smart Grid network is that companies are spanning across

multiple layers within the industry. Due to the industry’s maturity coupled

with the decade long partnerships among several of the industry’s main players,

the energy industry has traditionally been almost incestuous in its growth.

Basically, larger players will swallow up smaller players to take advantage of

their expertise and increase the company’s vertical integration within the

industry. For example, Siemens recently signed an agreement to acquire all of

the stock of eMeter Corporation. With this acquisition, eMeter will become part

of the Smart Grid Division of the Siemens Infrastructure & Cities Sector

and will become Siemens’ center for meter data management. (http://www.environmentalleader.com/2011/12/07/siemens-to-buy-emeter/)

However, as Smart Grid networks are built-up,

we’re seeing increased activity of new players entering the market, especially

at the consumer-facing level. Several competitions throughout the world offer

incentives for young entrepreneurs to build clean technology startup companies.

For example, the Cleantech Open has fostered such companies as ByteLite, NextGenEn, Inc. and Qado Energy. Will the small companies

continue to be acquired, or will Smart Grid be dominated by small players? We

predict that it will be a combination of acquisitions and partnerships over the

next five years that drive this industry.

Subscribe to:

Comments (Atom)